All of these services accumulate when you employ a bank, account maintenance fees, wire transfers, and check processing all accumulate. The fees escalate as you become more reliant on these services. Still, could we recover some of these costs? Fortunately, one can use the Earnings Credit Rate to lower these costs.

A crucial idea in the financial sector, it is often overlooked in the others. It is a major factor determining the general profitability and financial situation of a bank. ECR is used by businesses and financial analysts to evaluate performance; however, just what is it? More importantly, how does it affect you as a bank customer?

The idea of Earnings Credit Rate will be dissected in this paper along with an examination of its relevance and a justification of its computation. Understanding ECR will let you, regardless of your kind of company owner personal or corporate make wise financial choices.

What is the Earnings Credit Rate?

The ECR indicates a bank’s profitability, more especially, its capacity to generate interest revenue from its assets. Simply said, it displays the relative earnings of a bank from the money it loans or invests against the whole value of its assets. It is a major factor influencing the whole financial performance of a bank and shows the effectiveness of asset use.

Strong financial health is indicated by a higher ECR, which suggests the bank is generating more interest revenue per dollar of assets. Conversely, a reduced ECR might indicate either a lot of non-performing loans or inefficiencies in producing returns from assets.

Earning Credit Rate: History

The Earnings Credit Rate originated with Regulation Q, which prohibited banks from paying interest on deposits in checking accounts. Following the 1933 Glass-Steagall Act, the ECR aimed to limit loan sharking and other predatory actions. The act facilitated consumers to transfer funds from checking accounts to money market funds, leading to banks offering “soft dollar” credits to offset banking services.

Typically, the ECR is applied against “collected” balances, not “ledger” or “floating” balances, as these items are not available for transfer or investment. Collected balances are what has cleared and are available to transfer or invest.

Major Learnings

- Employing the interest income produced on its assets, ECR evaluates the profitability of a bank.

- A higher ECR points to more effective management and asset quality.

- It is affected by elements like loan quality, interest rates, and managerial effectiveness.

- ECR offers insightful analysis of the general stability and financial situation of a bank.

Clarifying the Earnings Credit Rate

Consumers utilizing ECR-linked financial products generally pay less for services. Some of these services are company loans, store services (like handling credit cards and balancing checks), cash management, wages, and checking, savings, debit, and credit cards. Customers may reduce service expenses using ECRs.Idle bank account money may create ECRs, lowering banking expenses. By increasing balances and deposits, banks may cut expenses and pass on savings to account holders. Most U.S. business account analysis and billing statements use ECRs to save costs.

Banks may independently establish earnings allowances, determining credit earning rates. Depositors only pay for services they utilize, yet it may dramatically lower bank service costs.

Interest Income

Interest income is money a bank gains from asset investments or loan proceeds. This covers loans given to people and companies, and profits from stocks or bonds as well as from its financial operations, the bank makes greater profit the higher the interest income.

Total assets

Including cash, loans, and investments, total assets represent what a bank holds. These cover securities kept, loans paid out, and other kinds of riches. A greater overall asset value suggests more bank activities and resources available.

Usually a good indication, a higher ECR suggests that the bank is producing more interest revenue concerning its assets. On the other hand, a lower ECR might indicate that the bank has a lot of non-performing assets or that it is having difficulty making enough returns on its assets.

Special Thoughts

Although it is a useful instrument for evaluating the financial situation of a bank, several considerations should be given:

Interest Rate Environment

The Interest Rate Environment is Rising interest rates let banks charge more on loans, hence perhaps improving their ECR. On the other hand, since banks make less on their assets when interest rates fall, the ECR might decline as well.

Loan Quality

Directly influencing a bank’s Earnings Credit Rate is the quality of loans it carries. Since non-performing loans (those unlikely to be repaid) either provide little or no revenue, a large number of them may lower the ECR.

Bank Management

In Bank Management By maximizing asset allocation, controlling risk, and negotiating reasonable conditions with borrowers, good bank management may assist in raising ECR.

ECR against Hard Interest: What distinguishes them?

Differentiate the ECR from hard interest rates:

Earnings Credit Rate (ECR)

An all-encompassing assessment of a bank’s general profitability with an eye on asset-generated interest income efficiency.

Hard Interest

Refers to the particular interest rate loan or other financial instrument charge is paying. It is a percentage applied to the principal amount and included in the ECR computation generally.

Although hard interest influences the Earnings Credit Rate, their application and goal differ. ECR presents a more all-encompassing assessment of a bank’s financial situation.

ECR vs Interest Earned

Notable differences also exist between Interest Earned and Interest Rate:

Interest Earned: The total monetary value a bank receives from loans and investments.

Interest Rate: The percentage charged on loans or credit. It’s a key factor in determining the bank’s Earnings Credit Rate but doesn’t encompass all variables.

ECR for Banks: Concerning Financial Implications

The Earnings Credit Rate is a key indicator for banks guiding choices about asset management, profitability, and risk control. Investors use it to evaluate the bank’s stability bank executives use it to make strategic loan portfolio and asset allocation choices.

While changes in ECR might point to underlying problems with asset management or market circumstances, a consistently high ECR indicates that the bank is in excellent financial health.

Calculating the Earnings Credit Rate

Earnings Credit = Average Daily Balance x Earnings Credit Rate × Number of Days in Period / 365. This formula yields the monthly earnings credit in dollars, which may be used to offset costs.

Example: If your business:

Averages $10,000 in account balance

Due $50 in service fees

If your bank’s ECR is 0.5% each year, compute the earnings credit: Credit for monthly earnings = $10,000 x 0.005 (30/365) = $4.11. As you can see, the savings are small. After using the earnings credit of $4.11, you’d still owe $45.89 in fees since the service costs are $50.It lowers banking expenses for firms with bigger accounts. Keeping your finances provides a discount on services.

Examining a Portfolio Account

Certain banks provide Portfolio checking Accounts, which provide consumers with better deposit interest rates than regular checking accounts. These accounts enable banks to boost interest revenue, hence improving their Earnings Credit Rate. Competitive returns on their deposits help consumers; banks increase their profitability ratios instead.

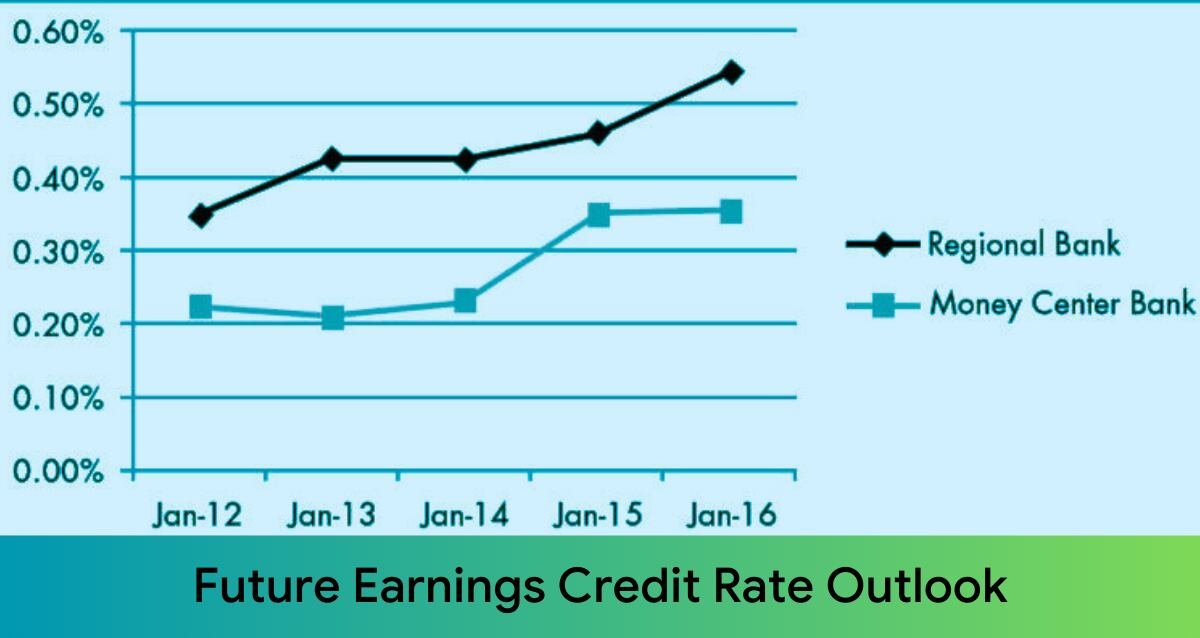

Future Earnings Credit Rate Outlook

Digitalization, legislative changes, and changing interest rates will all greatly affect the Earnings Credit Rate as the banking sector advances. Automation and artificial intelligence, among other technological developments, will help banks simplify processes and enhance asset management. However, rising fintech company rivalry and legislative pressure will drive banks to allocate their assets more strategically. Banks must react fast to these developments, modify their financial plans, guarantee better asset use to be profitable in this competitive market, and have their Earnings Credit Rate either maintained or improved.

How ECR may help your company

The Earnings Credit Rate may be very important for companies depending on banks for loans and financial services to ensure suitable conditions. The following is how:

Reduced Costs: High ECR banks might provide loan interest rates that are cheaper, therefore lowering the borrowing expenses for companies.

Better services

Financial stable institutions may make investments in improved customer services, therefore streamlining banking and increasing its convenience.

Enhanced Stability:

A strong Earnings Credit Rate implies a financially sound bank, therefore lowering the danger of instability or collapse.

ECR’s Limitations

The Earnings Credit Rate has restrictions despite its importance:

Earning credit rates range

It is calculated differently by banks. Big banks like money center banks provide lower average balance companies with higher ECR rates. This tactic draws clients. Regional banks lean toward businesses with greater average deposits. To devoted customers, they provide better ECR. Variance in alternatives and preparation makes them challenging and time-consuming.

Only certain fees

Depending on your bank, it generally covers transactional and maintenance expenses. Earnings credits may not repay special service fees, loan interest rates, or overdraft fees.

Benefit without cash

Maintaining a better balance can help you to get ECR credit discounts. These coupons cut bank expenses, but they are not cash.

You cannot carry over or remove your fees should they be less than your monthly credits. The key is to optimize your banking services using them.

High balances required

ECR pays more from higher balances. For many companies, especially smaller ones with limited cash flow or seasonal income fluctuations, this might not be feasible.

Smaller businesses might find it difficult to maintain a high balance given limited resources and operating restrictions. A company with erratic cash flow might also find it difficult to have a good average balance all year long.

Conclusion

An essential indicator of a bank’s capacity to generate interest revenue from its assets, the Earnings Credit Rate offers information on the financial effectiveness of the bank. Knowing the ECR will help consumers and companies decide which banks they should trust with their money in a more informed manner. It provides insightful data on a bank’s profitability, it is advisable to assess it in context with other financial indicators like asset quality, risk management, and liquidity to provide a complete picture of a bank’s general performance and situation.

Frequently asked questions

1. What is the Earnings Credit Rate?

Calculated by dividing a bank’s interest income by its total assets, the Earnings Credit Rate gauges the profitability of its assets.

2. How will ECR impact consumers?

A high Earnings Credit Rate indicates that a bank is in strong financial shape, which may lead to improved financial products for consumers and more competitive interest rates.

3. Can one find their own ECR?

Although the Earnings Credit Rate is a bank-level indicator, people gain indirectly from improved banking services and products from financially sound banks.

4. What affects the ECR of a bank?

Elements like loan quality, interest rates, and managerial effectiveness influence the ECR of a bank.

5. Is a high ECR always a positive indicator?

Although a high ECR must normally indicate something favorable.

Thank you for exploring our Blog! For additional captivating content, feel free to explore the website.